ICRA: Large, organised realty players better positioned to tackle Covid-19, expect significant acceleration in market consolidation

While cash flows in FY2021 are likely to be adversely impacted, balance sheet strength and liquidity are expected to be the key differentiators for these players

Covid-19 has served a double whammy to the already reeling residential real estate sector in India. With inflows from both new and already booked sales having been adversely impacted, stress levels on developer cash flows have increased. Sectoral demand has witnessed considerable moderation and committed sales receivables have slowed down due to deferment of mile-stone based payment demands, given the lower pace of execution, and delay in payments by some buyers on account of economic uncertainties. On the supply side as well, new launches have slowed down, and execution of ongoing projects has gotten hampered due to reduced labour presence and raw material supply chain disruptions. As per ICRA’s analysis, large realty players with established market positions, strong balance sheets and adequate liquidity have weathered the storm better than smaller players, who have been finding it difficult to cope with the prevailing market conditions. Consequently, the already ongoing consolidation of the sector is expected to accelerate further, with larger, more established players gaining increased market share.

Commenting on the same, Ms. Mahi Agarwal, Assistant Vice President and Associate Head at ICRA, said, “Home-buyers had already been leaning towards developers with an established track record of on-time and quality project completion, which had resulted in large, listed players reporting healthy sales and collections till 9M FY2020, despite the prevailing liquidity crisis and unfavourable supply-demand dynamics. The performance of these players was, however, adversely impacted by Covid-19 in Q4 FY2020, with Y-o-Y sales dropping by 11% in volume terms. Notably though, this decline remained significantly lower than the 30-40% Y-o-Y reduction witnessed in sales across key markets at an overall industry level. Collection levels for these larger, organized developers also remained stable. Their strong market position, together with their ability to switch to digital mediums for generating sales and maintain a positive customer experience, underpinned their relative resilience to the effects of the pandemic. Going forward as well, their balance sheet strength and liquidity are expected to keep them better-positioned to absorb the cash flow disruptions arising from the outbreak.”

Exhibit 1: Trend in Key Sales and Collections Metrics for ICRA’s Sample Set of Nine Listed Entities[1]

| Particulars | Q4 FY2020 | Q4 FY2019 | 9M FY2020 | 9M FY2019 | FY2019 | FY2020 |

| Area sold (mnsq.ft) | 10.06 | 11.26 | 23.43 | 21.89 | 33.15 | 33.49 |

| Y-o-Y growth (%) | -11% | 45% | 7% | 39% | 41% | 1% |

| Value of area sold (Rs Cr) | 6,328 | 6,951 | 15,630 | 14,073 | 21,025 | 21,958 |

| Y-o-Y growth (%) | -9% | 37% | 11% | 32% | 34% | 4% |

| Collections (Rs Cr) | 5,227 | 5,191 | 13,718 | 13,629 | 18,819 | 18,945 |

| Y-o-Y growth (%) | 1% | NA | 1% | NA | NA | 1% |

ICRA notes that with the longer period of disruption in Q1 FY2021 however, sales and collections metrics are likely to show a higher impact relative to Q4 FY2020, both for listed players, as well as for the industry as a whole. The ongoing economic uncertainties have led to reduced discretionary demand from home-buyers, and also resulted in an increased focus on conserving liquidity, leading to deferment of new purchases and delays in meeting payment demands raised by developers in recent months. Although certain developers with adequate project portfolio flexibility have responded to the slow-down by making payment structures more attractive and offering sales schemes in order to offload unsold inventory, a significant reduction in the overall sales traction remains likely. Cancellations are also expected to increase, especially for more recently launched projects with lower customer advance build-up.

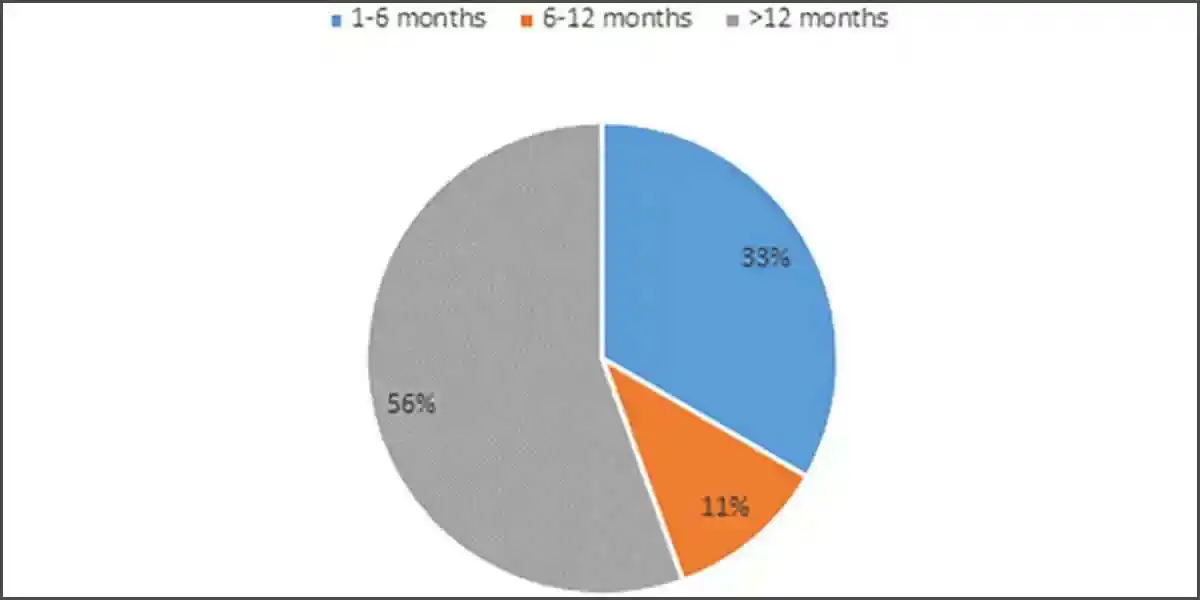

Thus, overall operating cash flows for most developers, including the listed players, are expected to witness significant moderation in the current year, resulting in increased reliance on available liquidity and/or refinancing to meet committed outflows. The larger, organized players have, however, maintained considerable liquidity buffers, mostly in the form of free cash/liquid balances and undrawn bank lines, which can be used to meet debt obligations, despite a reduction in collections and operating cash flows, although the undrawn bank lines may have some conditions associated with disbursement. The coverage on debt obligations from cash and liquid balances alone is sufficient to meet more than the entire year’s principal and interest payments for around 56% of ICRA’s sample set of listed players. Moreover, most of these developers also have low levels of leverage and enjoy high financial flexibility, which would provide significant support in managing event-related shocks.

Exhibit 2: Cover on Debt Obligations from Cash Equivalents for ICRA’s Sample Set of Nine Listed Entities

“Notwithstanding the adverse impact of Covid-19, most large organized players with established brands, low leveraged balance sheets and adequate liquidity are expected to benefit from the likely acceleration in consolidation in the residential real estate segment. Range bound prices and low home loan rates are also expected to further support sales for these players once the impact of the virus begins to recede. The players who are able to weather this storm are likely to focus on phase-wise launches going forward, with de-densification of housing projects becoming a key part of project plans. The creation of business centres / work areas within residential complex may also become a focus area,” added Ms. Agarwal.

Published on:

16 July 2020

Share:

We Value Your Comment