India Ratings Flags Rising Input Costs Risk for Cement Sector Amid Gulf Crisis

Ind-Ra opines that the Gulf crisis is likely to be reflected in higher input costs during 1QFY27 once existing inventories are depleted. However, the impact on EBITDA/tonne would remain contingent on companies’ responses. Tier-2 players, with structurally weaker balance sheets and limited diversification, may face sharper margin pressures.

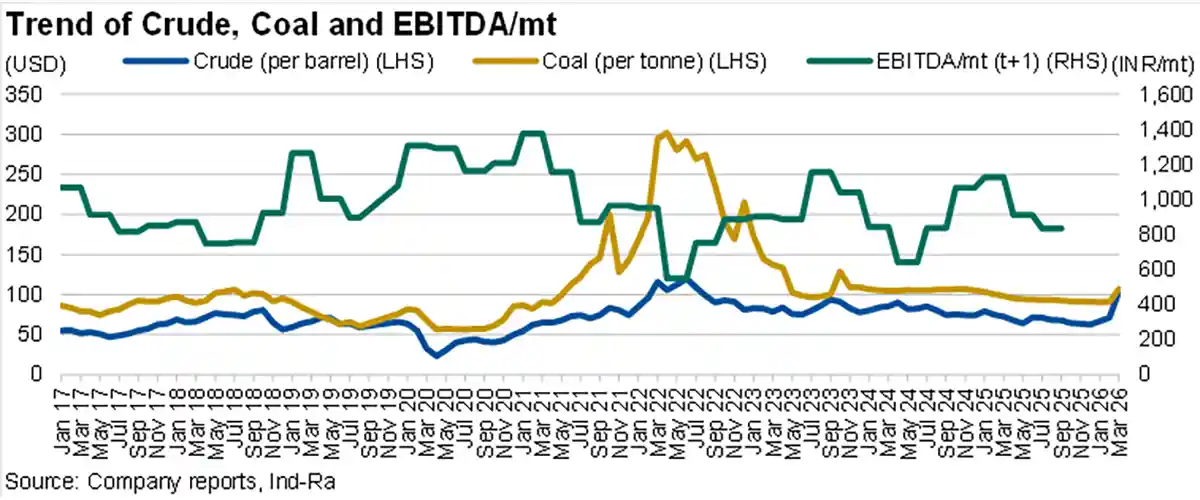

Pricing Power Key as Gulf Crisis Fuels Cost Pressures; Tier 2 Players Vulnerable: Ind-Ra expects the sharp price increase in coal and pet coke will start reflecting in the overall EBITDA/tonne in 1QFY27, currently cushioned by existing inventory. Freight cost is sensitive to domestic diesel prices. “While delivered coal prices increased in double digits in March 2026, the increase in pet coke prices is sharper, as disruptions to refinery operations and shipping flows from the Middle East have tightened the supply. Resultantly, high calorific value coal is emerging as a more competitive option than pet coke, and the fuel mix of cement players is likely to swing towards coal over the near term. Additionally, packing material costs have risen sharply, though their impact on overall profitability would remain limited as they account for 2%–4% of the total costs. Resultantly, cement companies could witness an increase of INR175-200/mt in the total costs over 1QFY27, necessitating a mid-single digit increase in prices to maintain profitability levels”, says Khushbu Lakhotia, Director, Corporate Ratings, Ind-Ra.

Cement prices typically move in a narrow low-to-mid single-digit band, given the range-bound capacity utilisation, as evidenced in 2022 when fuel prices soared during the Russia-Ukraine conflict. The ability of the industry to undertake price hikes amid the elevated competitive intensity and a decadal-high supply pipeline will be the key determinant of EBITDA over the next few months. Tier‑2 players remain more exposed as limited buffers heighten sensitivity to these cost escalations. EBITDA/mt improved 25% to INR950 in 9MFY26, aided by price hikes, benign input costs, and better operating leverage. Ind-Ra expects industry profitability to recover in FY26.

FY26 Demand Momentum to Hold Steady: Ind-Ra expects cement demand to have grown around 8% yoy in FY26, supported by strong infrastructure spending and a resilient housing demand. The robust 8%-9% demand growth in 11MFY26 and double‑digit demand expansion in 3QFY26 indicate continued momentum, despite a high base in 4QFY26. Although cement prices softened over 2Q-3Q with the monsoons and GST rate cut, realisations are likely to stabilise in 4QFY26, translating into a modest low‑single‑digit increase for the full year. Sequential price improvements in 4QFY26 should support realisations, though Tier‑2 players may experience softer pricing due to regional competition.

Capacity utilisations are likely to have improved sequentially in the seasonally strong 4Q, aided by the peak construction activity. However, with the substantial pipeline of new capacities scheduled to come online, Ind‑Ra expects utilisation levels to remain broadly stable on a yoy basis in the near term, as incremental supply tempers any sharp improvement from current levels.

Published on:

03 April 2026

Share:

We Value Your Comment