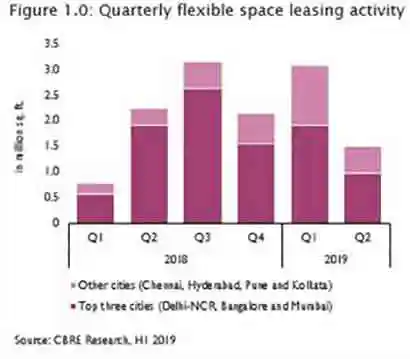

Flexible Space Take-Up In India Reaches 4.6 Million Sq. Ft. In H1 2019

Commenting on the findings of the report, Anshuman Magazine, Chairman and CEO, India, South East Asia, Middle East and Africa, CBRE, said: "India is currently one of the leading flexible space markets in APAC and we expect increasing investments in this segment going forward. Office stock is expected to grow from 600 mn sq. ft. in mid-2019 to a billion sq. ft. by end of 2030 and flexible space will comprise 8-10% of the total office stock".

Flexible space stock crossed 50 million sq. ft. across leading cities in APAC during Q1 2019; in India, this stock exceeded 20 million sq. ft. This consistent growth in the country was a result of operators leasing medium- to large-sized spaces across cities.

Mr. Ram Chandnani, Managing Director, Advisory and Transaction Services India, CBRE, said, "Customized enterprise solutions provided by operators offer a competitive advantage as well as enable them to retain tenants for a longer term. This is expected to continue to attract established corporates towards the flexible space segment."

Some of the key trends visible in H1 2019 include:

Increasing occupancy rate – This is primarily a result of established corporates leasing large-sized spaces in recent times, in order to provide 'free addressing' options as well as improve agility of their RE portfolios.

Penetration into tier II cities – Operators have turned their focus from the top seven cities to tier-II cities such as Jaipur, Goa, Chandigarh and Lucknow in the past few quarters.

OUTLOOK

CBRE expects operators to continue taking up large sized spaces (> 100,000 sq. ft) across cities, moving beyond the top cities to cover other major markets and tier II cities as well. This will continue to strengthen the overall space take-up. Also, the continuously increasing demand for space in non-core micro-markets, coupled with paucity of space in core micro-markets, is likely to result in the former dominating leasing in the future. We also expect the demand for managed office spaces will strengthen in the coming few quarters and become almost comparable to that of hybrid spaces. Moreover, we anticipate this segment will remain high on the investors' radar.

Published on:

22 August 2019

Share:

We Value Your Comment