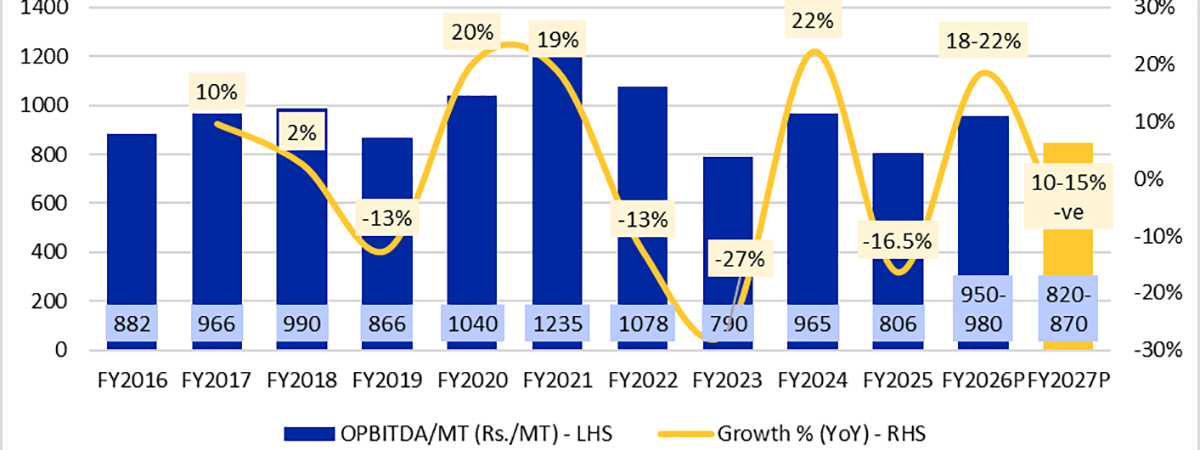

Rising Input Costs Amid West Asia Tensions to Weigh on Cement Sector Profitability In 2026-27: ICRA

Giving more insights, Anupama Reddy, Vice President and Co-Group Head, Corporate Ratings, ICRA, said: “The crude-linked cost pressure poses a key risk, particularly if geopolitical tensions persist. In 2026-27, power and fuel costs are set to rise, driven by the uptick in petcoke prices, tightening fuel markets and likely rise in coal prices. Additionally, higher logistics costs and a depreciating rupee are expected to increase the landed cost of fuel. Overall, power and fuel costs are likely to increase by 10-12%, while selling costs could rise by 6-8% in 2026-27, owing to higher freight and packaging expenses. The cement companies, however, are expected to mitigate a part of the impact through price pass-through, thereby cushioning the overall profitability.”

The sector is highly dependent on coal/petcoke for clinkerisation and operating captive thermal power plants, reflecting its energy intensive nature. From a distribution perspective, the cement companies mainly rely on road networks for transportation of cement to end customers as well as for the movement of raw materials to manufacturing facilities.

Crude oil prices have surged owing to the West Asia conflict and closure of the Strait of Hormuz. The prices are likely to stay elevated if the war prolongs. ICRA expects crude price to average $95/bbl in 2026-27, in the baseline scenario, compared to ~$72/bbl in 2025-26. Petcoke prices have already risen sharply, with a 19% MoM increase in April 2026, and diesel prices have gone up by Rs. 3.9/litre in May 2026.

“Pricing flexibility of the cement players continues to remain constrained due to intense competition. Cement prices are expected to increase by 3-5% in FY2027, following a marginal recovery of ~2% in FY2026. Industry players have initiated price hikes of Rs. 10-12 per bag in April 2026, although the extent of cost pass-through remains contingent on demand-supply dynamics. Despite cost pressure, the sector’s credit profile remains stable and debt protection metrics are likely to remain comfortable,” Reddy added.

Published on:

21 May 2026

Share:

We Value Your Comment