From Local Assembly to Global Leadership India’s Construction Equipment Industry on the Rise

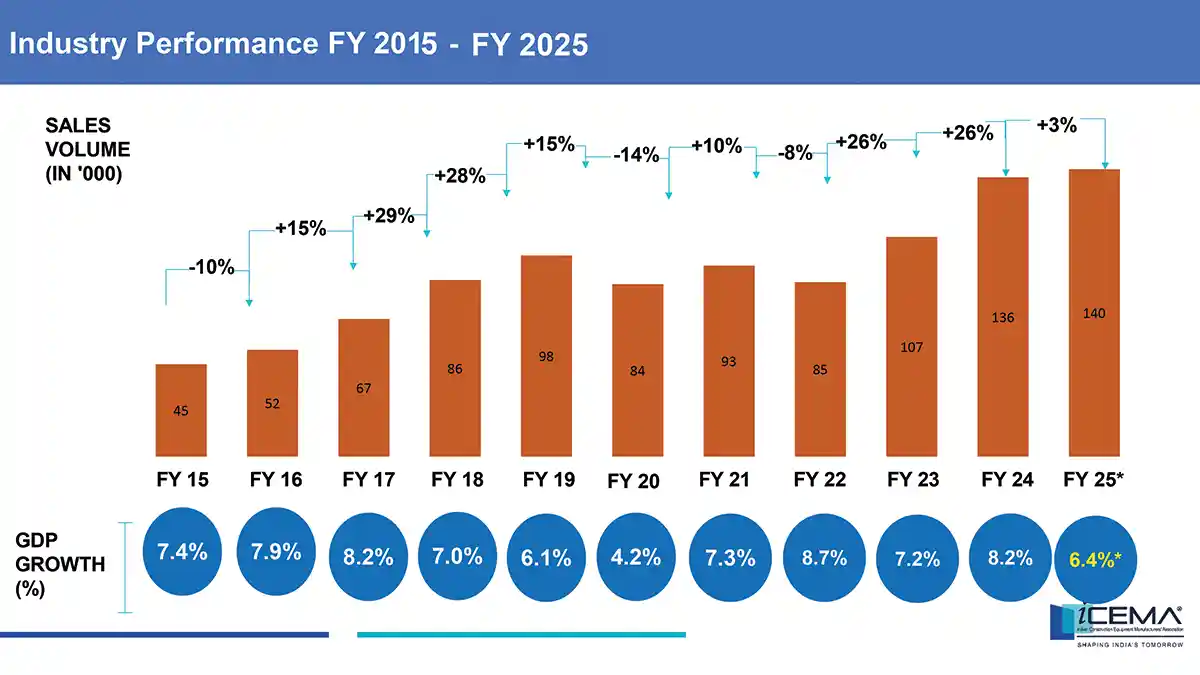

India’s construction equipment (CE) industry is cementing its status as a thriving hub for manufacturing and exports, riding on robust infrastructure investments, smart technologies, and rising global demand. From earthmoving to road construction equipment, crushing and sand washing to material handling systems, made-in-India machines are powering projects across continents, symbolizing the country’s rise as a global manufacturing force.After an extraordinary 26% surge in CE sales in FY23 and FY24, the CE industry’s value has swelled almost threefold — from an estimated US$3.5 billion in FY2013-14 to about US$10 billion by FY2023-24. This growth moderated to about 3% in FY25 with 1,40,191 units sold (as per ICEMA), compared to 1,35,650 units sold in the previous fiscal year. The slowdown in sales was largely due to the general elections, new emission norms, and the late monsoons, despite which, the industry remained resilient as was evidenced in the 10% jump in exports in FY25, which helped offset softer domestic demand, reinforcing India’s position as the world’s third-largest CE market.

S.A. Faridi

Managing Editor

Though demand remained sluggish in the first half of FY26, optimism runs high among policymakers and industry leaders who believe India is well on course to become the world’s second-largest construction equipment market by 2030–2032, with annual sales expected to touch nearly 2,50,000 units. The industry is betting on a strong rebound in the latter half of the fiscal year, fuelled by renewed economic momentum and a fresh wave of project awards slated for the coming months.

The following sections examine the key drivers of this growth, the evolution of indigenous manufacturing, India’s strategic advantages for global OEMs, its expanding export footprint, strengthening of local supply chains, and how policy and technology are shaping a sustainable, future-ready CE ecosystem.

Key Drivers of Domestic Demand

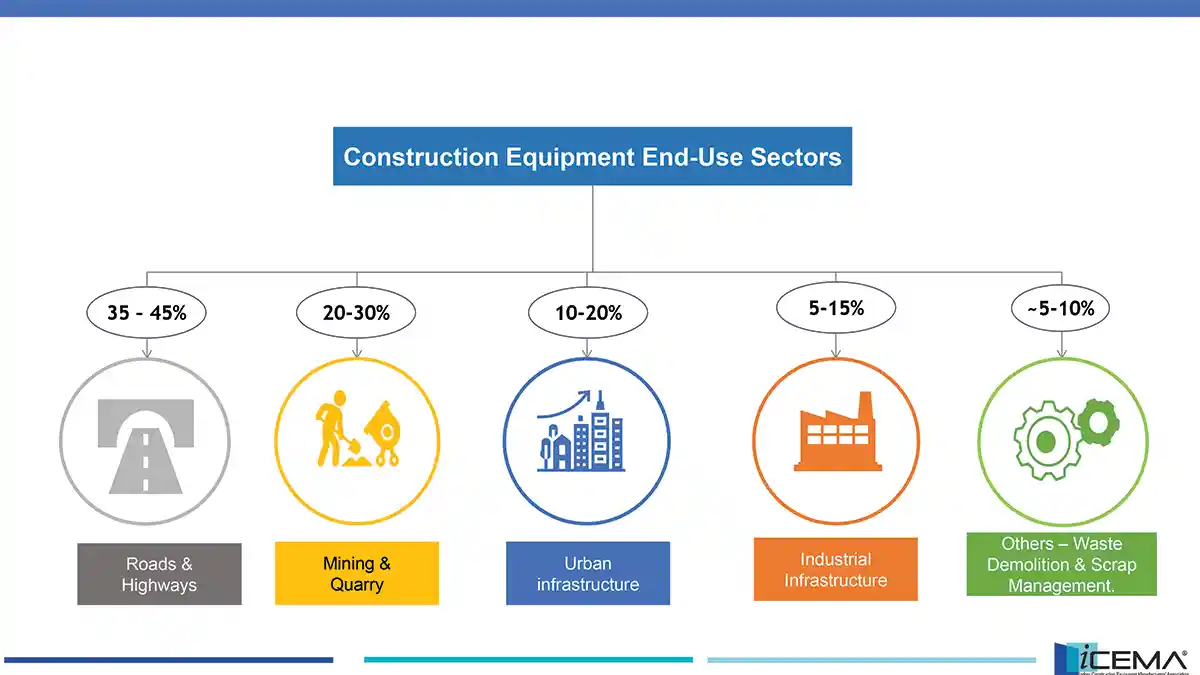

Key sectors in the Indian economy help drive the CE sector, as do large scale government programmes and initiatives for infra development. The government’s infrastructure push, underpinned by record budgetary allocations and programs like the National Infrastructure Pipeline (NIP) and PM Gati Shakti, and increased public spending, has sustained a strong momentum in the sector.Road construction projects continue to be the single largest demand driver, accounting for nearly 40% of India’s construction equipment market. The government’s commitment to award 9,000 km of new road projects by the end of this fiscal year, coupled with efforts to cut the time between project approval and commissioning by almost a year, is expected to significantly boost equipment demand in the second half of FY26.

The mining sector is also influencing the CE industry’s growth trajectory, contributing around 25% of CE sales, while the real estate sector accounts for another 15%. The outlook for the next fiscal will largely depend on how effectively the infrastructure budget is implemented, with faster on-ground execution emerging as the decisive factor for sustaining growth (Figure 1).

Figure 1:

The rural economy, buoyed by development programs such as PMGSY and PMAY-G which focus on rural roads, housing, irrigation, and water supply, have spurred the need for purpose-built machines like backhoe loaders, mini excavators, and telehandlers, tailored to work in diverse terrains, and meet the requirements of smaller contractors, thereby broadening the market base. At the same time, the resurgence of sectors like railways, industrial construction, and renewable energy is also propelling demand across the CE industry.

Meanwhile, localization and Make in India initiatives are bolstering domestic production capacity, enabling quicker deliveries and cost competitiveness, and stimulating demand.

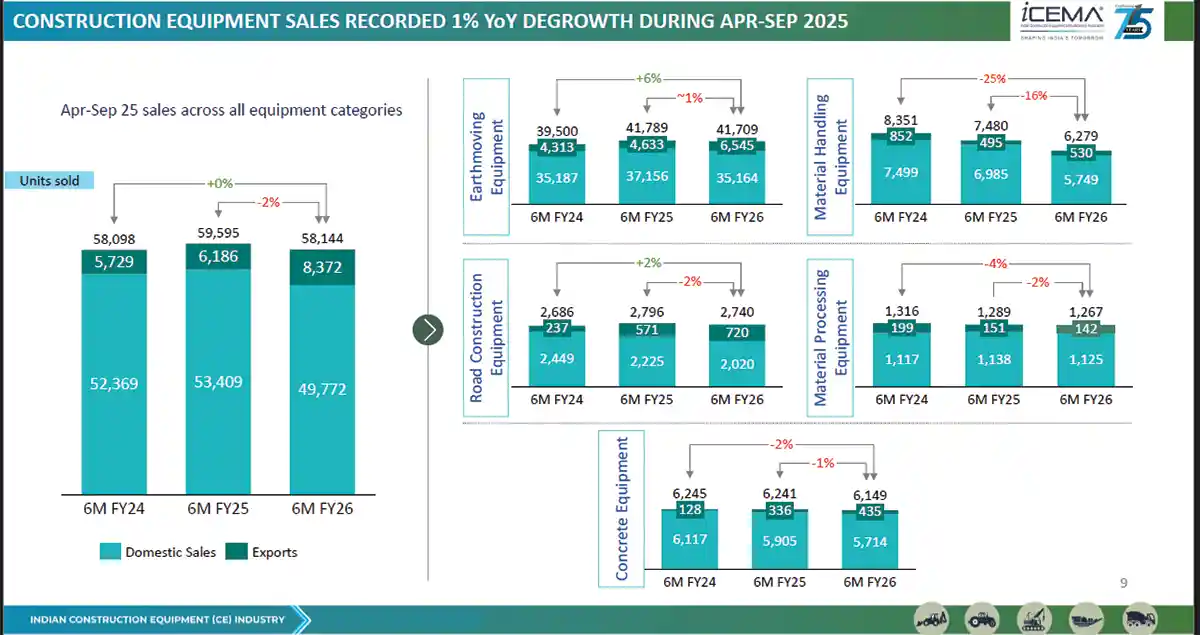

India’s CE industry notched record-high sales of over 1,35,000 units in FY24, and although it saw only modest growth to 1,41,000 units in FY25, it remained on a high plateau of activity. Figure 2 captures the recent half-yearly trends, reflecting a slight dip in early FY26 amid the impact of general elections, seasonal factors, and policy headwinds, while also highlighting the growing divergence between domestic and export performance.

In the first half of this fiscal, overall volume fell 2% on-year, with a 35% jump in exports mitigating the drop in domestic demand to some extent. The drop is largely due to the slowdown in road construction, a key demand driver, which is expected to ease to 23–25 km per day this fiscal from 34 km in fiscal 2024, reflecting weaker project awards, an erratic monsoon, stabilising real estate activity, and higher equipment costs. The monsoon extended into October.

Looking ahead, the consensus is that India’s CE upcycle is intact, provided policy momentum translates into timely project execution. Rating agencies ICRA and CRISIL project a 2–5% volume uptick in FY26 (to ~1.45 lakh units) assuming a pickup in project awards in H2. Crucially, the industry’s focus has expanded beyond chasing volumes; it is now equally committed to innovation, localization, and sustainability as long-term growth pillars. The 35% surge in exports during the first half of this fiscal was largely driven by rising demand from Africa and Latin America.

Figure 2:

The rollout of CEV-V emission norms in January 2025, which align domestic equipment with global standards, has opened access to advanced markets such as Europe, North America, and Japan, where cost efficiency and regulatory compliance are crucial. India’s ability to capitalise on these opportunities amid ongoing geopolitical tensions will be critical, even as steady demand from traditional markets continues to keep exports resilient.

Evolution of CE Manufacturing in India

The growth trajectory of CE manufacturing in India over the past decade has been remarkable. From being largely an assembly base, dependent on imported machinery and components in 2010, today, the CE industry has become a manufacturing hub for many global companies, with 98% of the construction equipment sold domestically, being produced in India now. The industry owes this indigenization to the government’s ‘Make in India’ drive and its enabling policies such as reduced import duties on parts, easier FDI norms, and ease of doing business initiatives.Importantly, India’s manufacturing ecosystem has matured in capability. Leading OEMs like JCB, Caterpillar, Komatsu, Tata Hitachi, Kobelco, HD Hyundai, Schwing Stetter, Sany, Volvo, Terex, Escorts Kubota, Conmat, Puzzolana, Manitou, Propel, and many others operate state-of-the-art plants in India which incorporate Industry 4.0 practices such as automation, robotic welding, and IoT-based quality control.

In fact, Indian engineering prowess can now meet international standards. For instance, domestic companies are now producing advanced piston pumps and axle components that were being imported five years ago. This has given MNCs the confidence to base more of their production and even their R&D divisions in India. This capability is also reflected in product developments with India’s CE industry having swiftly adopted CEV Stage IV emission norms and implementing Stage V early this year, putting it at par with Europe in environmental standards.

Figure 3:

Strategic Advantages for Multinational Corporations

Global construction equipment manufacturers find India an increasingly attractive destination --- not just to sell, but to invest and build for the world. One obvious advantage is the sheer scale and growth of the domestic market which gives volume certainty to manufacturers, even during global downturns. Despite a challenging global environment, India’s CE sector grew modestly in FY25 while other markets stagnated.Another advantage is our cost-competitive manufacturing. India offers a large skilled workforce with significantly lower labor costs than developed countries, and even China. For example, factory workers in India earn between $150 and $300 per month, while in China, wages often exceed $600 in industrial areas. Many OEMs report that Indian factories can produce equipment at 20-30% lower cost than in the Western plants, without compromising quality.

The supplier base is also deepening. India has a vast network of MSME component makers capable of producing castings, forgings, hydraulics, and sub-assemblies at competitive prices. The move towards improving productivity enabled by automation and training also make India an attractive manufacturing base.

Furthermore, policy reforms have enhanced India’s appeal. Stable policy direction on infrastructure (with NIP commitments through 2030) gives companies long-term visibility to invest in capacity. The government has also simplified regulations for joint ventures and technology transfer, and has introduced programs like the SAMARTH Udyog (Industry 4.0) to assist manufacturers in adopting advanced technologies.

What’s more, initiatives like setting up logistics parks, improved ports, and GST-led supply chain efficiencies have reduced the cost of both importing components and exporting finished machinery.

Crucially, India’s push towards sustainable and innovative tech aligns with global OEMs’ own strategic goals. Global OEMs like Caterpillar, Komatsu, Volvo, etc see India as a test-bed for frugal engineering and green innovation. Another progressive development being leveraged by multinational corporations is India’s improving intellectual property regime and innovation ecosystem. The rise in patents filed from India’s engineering centers and collaborations with local tech startups (for AI, IoT applications in CE) demonstrate that MNCs can co-create cutting-edge solutions in India. All these advantages, market size, cost efficiency, supportive policies, focus on sustainability, and innovativeness in the CE industry, are making India a linchpin in the growth strategies of CE giants.

However, businesses have raised concerns about bureaucratic delays and complex tax regulations ('tax terrorism’). To address this, the government should further simplify compliance and improve transparency, making India a more business-friendly destination.

Figure 4:

Expanding Global Footprint

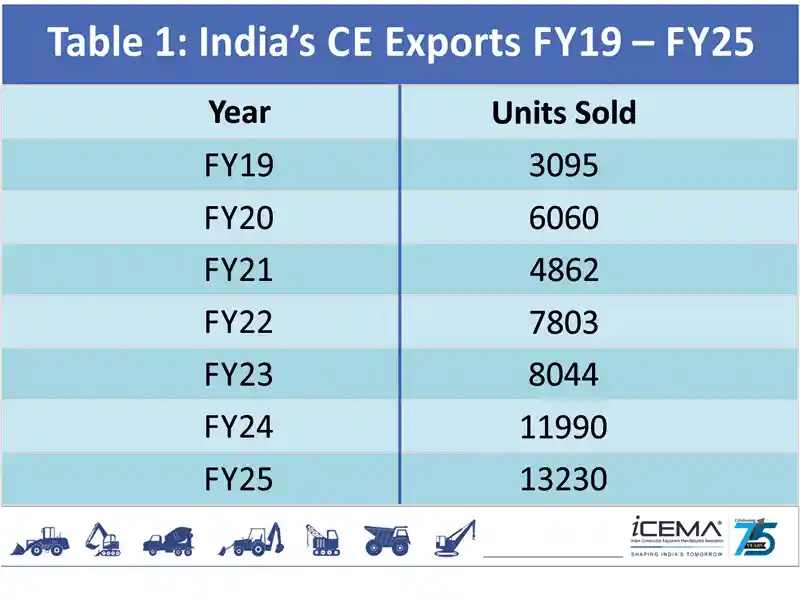

India’s equipment industry is no longer confined to meeting domestic needs; it is increasingly making its mark worldwide. Over the past few years, export of construction equipment from India has surged sharply, reaching 13,230 units in FY25 (up 10% YoY) after an even bigger 49% jump in FY24. Indian-made backhoe loaders, excavators, cranes, and concrete pumps are now operating in over 120 countries. Primary markets include the Middle East, Africa, South-East Asia, and North America, with Europe, Latin America, and the Stan countries also seeing growing penetration (Figure 4 and Table 1).

The Indian government and industry bodies are actively encouraging this outward thrust. ICEMA’s Vision Plan 2030 aspires to raise exports to ~25% of the industry’s output by 2030 (from ~10% currently), which could equal US$3 billion in CE exports. To achieve this, manufacturers are pursuing international certifications and customizing products for target markets (examples include special tropicalized cooling systems for Africa; engines meeting US EPA Standards for North America etc).

Trade agreements and diplomatic outreach also play a role. India’s growing economic ties in Africa and South Asia often include infrastructure cooperation, which opens doors for Indian CE exports. The ‘Development Partnership’ projects in countries like Nepal, Bangladesh, Kenya, and Myanmar frequently use equipment supplied by India, and even financed by Indian credit lines. Domestically, the government has discussed incentives like export financing support and faster GST refunds for exporters, to enhance competitiveness.

One can gauge India’s expanding global footprint by the fact that Indian OEMs now attend all major international trade shows (bauma, CONEXPO - CONAGG, WOC, etc). Joint ventures such as Tata-Hitachi and L&T-Komatsu are entrusted with global supply mandates for specific products. In 2024, L&T’s Chennai facility became a global sourcing hub for Komatsu’s smaller bulldozers, exporting to over 20 countries. ACE has reported double-digit growth in exports of its cranes and forklifts, and is setting up offices in Europe and the Middle East. There are many more examples like this.

Component exports are also a crucial part of India’s exports with Indian suppliers exporting engines, cylinders, and fabricated sub-assemblies for global production lines of Caterpillar, CNH, and others. Industry experts highlight that India still accounts for only ~1.2% of global CE exports, so the headroom is immense.

With the world looking for a ‘China-Plus-One’ sourcing alternative, India is well-positioned to capture a larger share of international demand, provided it continues to assure quality and timely delivery. While recognition of Indian manufacturing quality and competitive pricing has grown, the challenge now is to ensure consistent product support overseas and navigating trade policies. For instance, there have been concerns about potential reciprocal tariffs in the US, though the impact is expected to be limited by market diversification.

Overall, the trend is clear: India’s CE industry, once an import-dependent sector, is increasingly a net exporter. Its expanding footprint not only earns revenue but also elevates India’s stature as a global manufacturing hub of construction equipment, underpinning its ambition to emerge as a major exporter in this sector by 2035.

Strengthening MSMEs and CE Supply Chain

At the heart of India’s CE industry is a vast network of Micro, Small, and Medium Enterprises (MSMEs) that supply parts and sub-systems for equipment. In recent years, OEMs and policymakers have made concerted efforts to upgrade local suppliers’ capabilities, reduce import dependence, and build a greener, more robust value chain.A key development has been the consolidation and upskilling of the vendor base. For instance, Tata Hitachi reports that it halved its number of vendors over the past decade, focusing on those who could scale up and meet stringent quality standards. This development has, however, come under challenge from disruptive events like the pandemic and other geopolitical tensions which revealed the merits of diversification for resilience. ACE, one of the largest material handling and earthmoving equipment companies, is also mapping critical components and ensuring diverse sourcing options, including nurturing second-tier suppliers.

Another focus area is localization of high-value components. Despite overall indigenization, India still imports precision parts like pumps, valves, electronics and undercarriage components in large volumes. To address this, ICEMA has proposed a dedicated PLI scheme for construction equipment components to incentivize investments in “mother technology” production (such as hydraulic systems and electric drives). Parker Hannifin India recently developed an advanced hydraulic piston pump indigenously, which is a major feat.

To further strengthen MSMEs, greater emphasis is being placed on skill development and technology transfer. Training initiatives on lean manufacturing, quality control, and advanced fabrication techniques are helping the MSMEs enhance productivity and meet global standards. Industry forums and government programs under the Skill India mission are also working to upskill the construction equipment supply chain workforce.

Access to finance for MSMEs is improving through schemes that facilitate quicker payments and easier credit, recognising that a financially sound supplier base is vital for the sector’s overall health. Strengthening MSMEs and the CE supply chain has thus become a multifaceted mission — aimed at reducing import dependence, improving reliability, cutting carbon emissions, and fostering innovation at the grassroots.

By investing in their supply chain partners, India’s construction equipment manufacturers are ensuring that the nation’s manufacturing ecosystem continues to grow stronger and more sustainable.

Ramping Up India’s Manufacturing Ecosystem

Building a world-class equipment industry requires more than factories and suppliers – it needs a holistic manufacturing ecosystem encompassing skilled people, innovation, and supportive policy. One critical component is human capital development. The CE sector will require an estimated 6 million skilled workers to operate and maintain machinery, staff factories, and manage projects. Recognizing this, ICEMA and allied bodies have ramped up training initiatives and many OEMs have set up operator training and skilling centers within their premises.A 2025 ICEMA Human Capital Trends report highlighted that the current educational curricula does not fully meet the construction industry’s requirements, especially in areas like equipment telematics, data analytics, and electric drivetrains. The industry is therefore partnering with technical institutes to update courses and provide apprenticeships. There is also a push for greater diversity and inclusion in the CE workforce, aiming to attract more women into engineering and shopfloor roles, which enlarges the talent pool.

The government’s support by way of industry-government collaborations and policies remain pivotal. Government authorities have worked closely with ICEMA on regulations like emission and safety norms for CE vehicles. Such collaborative approach was seen in the phased roll-out of CEV Stage V norms from 2024, giving the OEMs time to make the transition while ensuring that the environmental goals were met.

Long-term policy visibility has allowed companies to invest with confidence; steel and cement companies are expanding capacity anticipating infrastructure demand through 2040, which in turn signals CE manufacturers to scale up. However, challenges like land acquisition delays and state-level project slowdowns persist. Industry voices are calling for reforms in these areas, suggesting that streamlining clearances and enforcing project deadlines at local levels will significantly boost infrastructure execution, a win-win for development and CE demand.

Finally, technology and sustainability are the twin pillars strengthening the manufacturing ecosystem’s future. The Indian CE industry is undergoing a digital transformation in both product and process. Manufacturers are implementing smart factory solutions – IoT sensors monitor machine health on assembly lines, AI-driven analytics optimize production schedules, and automation is used for repetitive tasks to enhance quality.

Almost all new equipment now come with telematics and GPS for tracking and performance monitoring. Fleet owners can leverage these for preventive maintenance and efficiency gains. This digital leapfrogging not only improves current productivity but positions India as a leader in smart construction practices – a value-add that global investors and partners appreciate.

The infra construction and equipment manufacturing ecosystem is increasingly aiming to become more eco-friendly by moving toward low-carbon equipment and operations. All major OEMs in India have announced targets for reducing emissions: whether it’s shifting to renewable power in factories, improving engine fuel efficiency by 30-40% over the past decade, or introducing alternative-fuel machines. According to a report by MarketsandMarkets, the global market for electric construction equipment alone is projected to reach $13.5 billion by 2026, growing at a CAGR of 22.7%.

Conclusion

India’s construction equipment industry stands at an inflection point where its global aspirations are being met by an internal transformation. The convergence of strong policy support, public investment, technological innovation, skill development, and sustainable practices is creating an ecosystem capable of not only meeting India’s infrastructure needs but also exporting solutions to the world. The industry’s journey from being an import-dependent sector to a thriving export hub and innovation center is a microcosm of India’s broader manufacturing resurgence. Challenges remain, from ensuring consistent project execution to bridging the skill gap, but the trajectory is firmly upward.

Published on:

03 December 2025

Published in: NBM&CW DECEMBER 2025

Share:

We Value Your Comment