Indian Construction Equipment Market in 2022 & Beyond

Mayank Agrawal, Asst. Vice President & Sector Head, ICRA

The mining and construction equipment (MCE) industry contracted by 10-12% in CY2020 due to the pandemic-induced economic slowdown, which dragged sales by 39% in H1 CY2020, before a strong demand uptick of ~22% in H2 CY2020, which continued in Q1 CY2021.

ICRA estimates a 15-20% growth in CY2021. The industry is likely to continue with its growth trajectory till CY2023, before moderating in CY2024 as typically seen in years with general elections. Further, demand is expected to remain volatile amid a robust growth of around 55% in Q1 CY2021, followed by a subdued Q2 due to the second wave of the pandemic and the emission-related pre-buy pick-up and a post-buy slump in Q3 and Q4 of CY2021, respectively.

While the second wave was more widespread and impactful than the first one, a better prepared ecosystem, localized lockdowns, and limited movement of migrant labourers led to a relatively lesser impact. However, concerns related to subsequent wave of the pandemic, increasing prices of equipment and cautious financing environment may impact the overall demand. Nevertheless, a decline in new infection rate and improving pace of vaccination drive remain positives.

Support to ICRA’s equipment demand estimate originates from the Government’s continuing with its ‘Build India’ momentum to counter the economic slowdown. The road construction activity remains the largest driver of construction equipment (CE) demand with execution reaching record high levels of 13,327 km in FY2021, up 30% on a YoY basis, despite challenges from the Covid-19 pandemic and associated lockdowns.

Source: ICRA research; volumes for earthmoving (backhoe, excavators, wheeled loaders, skid-steer), road construction (compactors, pavers and motor graders), material handing (PNC), and mining (dumpers and dozers).

Source: ICRA research; volumes for earthmoving (backhoe, excavators, wheeled loaders, skid-steer), road construction (compactors, pavers and motor graders), material handing (PNC), and mining (dumpers and dozers).The per-day execution reached the highest level of 37 km in FY2021, with a target of 40 km per day in FY2022. New project awards increased by 23% in FY2021 to reach 10,965 km. Project awards are likely to remain at the similar level in FY2022, buoyed by the recent amendments to the HAM model as well as relaxation in technical and financial capacity for EPC and HAM contract awards. With the second wave of pandemic, the road execution moderated to 24 km per day during Apr-May 2021, though the impact remained limited due to localized lockdowns and the per day execution is expected to gain pace in the coming months.

Source: MoRTH, NHAI, ICRA research

Source: MoRTH, NHAI, ICRA researchFurther, the gross value added (GVA) of the construction sector recovered considerably in H2 FY2021, recording a sharp turnaround from the YoY contraction of 7.2% in Q2 FY2021 to a 6.5% growth in Q3 FY2021 (-1.3% in Q3 FY2020), before rising sharply to a series-high 14.5% in Q4 FY2021 (+0.7% in Q4 FY2020). This was in line with a recovery in the lead indicators such as production of cement, steel, and other key infrastructure/construction raw materials. Moreover, healthy project awards in the roads sector, a pick-up in execution as well as favourable policies from the Government in terms of lowering the Bank Guarantee requirement, faster clearance of bills, and speedier clearances/approvals supported a sharp improvement in this sector.

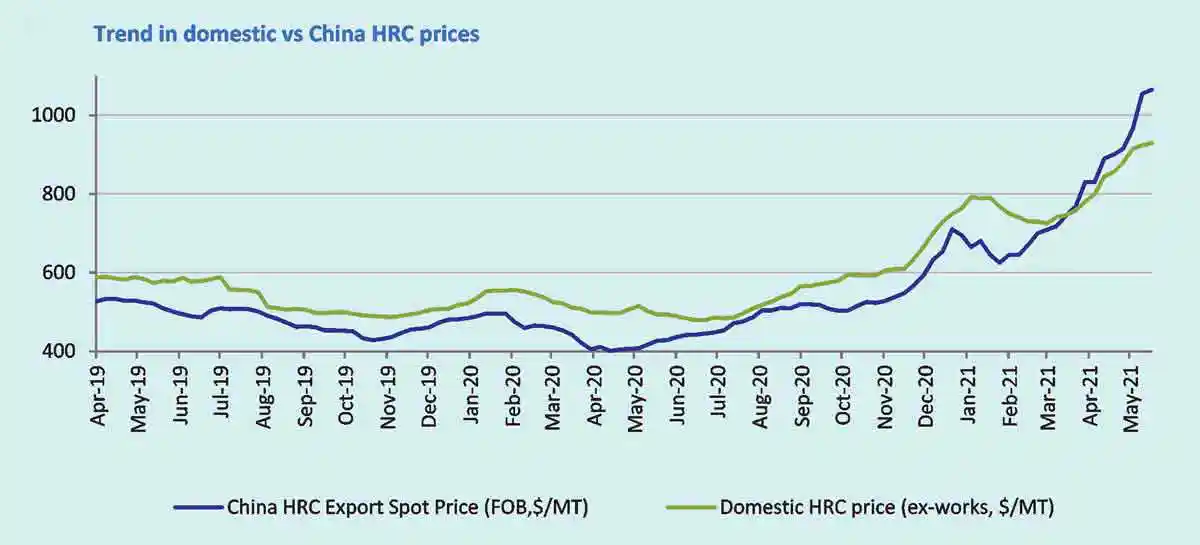

Nevertheless, what has been a mounting concern for the industry is the increase in input costs which will pressurize the profit margins in the current year. The domestic steel prices have been increasing consistently from July 2020 on the back of demand revival and an increase in international steel prices. Steel prices touched multi-year highs over the past few months and the current HRC prices hover at around Rs. 68,000-69,000/MT. Despite the hike, domestic HRC prices continue to remain at a discount compared to the current international rates with Chinese HRC prices around $945/MT in the third week of June 2021.

While many OEMs have already taken sequential hikes this calendar year, additional hike is warranted to neutralise this impact of sustained input price increase. Apart from supply issues, input costs for precision components, oxygen and international freight costs have already increased manifold.

The whole problem has been further exacerbated by new emission norms (CEV-III to CEV-IV from October 1, 2021) for which the OEMs expect around 10% hike in prices of the new compliant CEs. Further, after a robust demand in Q1 CY2021 and an expected pre-buying demand for CEVIII vehicles before cost hike, the OEMs have increased finished goods inventory.

Source: Steelmint, ICRA research

Source: Steelmint, ICRA researchThe sales of this stock have been slower than expected due to the second wave of the pandemic, leading to an increased carrying cost. The players have been taking tighter cost control measures and are expediating focus on indigenization to rationalize costs.

Further, ICRA expects that demand for the refurbished CEs will rise because of costlier higher complaint vehicles (CEV-IV). The CE operators will also require upskilling and get accustomed to new CEV-IV, which has more electrical control compared to CEV-III, which was more mechanical. Further, while the OEMs promise better engines and relatively lower maintenance cost over life of the new compliant vehicles, the full impact and success of the same will take time to be noticed.

Tighter financing approach by financial institutions is another challenge for the industry. As almost 90% of the CEs are financed by lending institutions, an upsurge in delinquencies due to the pandemic (which has shot up in the recent months due to the second wave of the pandemic) is a concern, especially owing to the absence of any moratorium this time. Already with one large NBFC going into NCLT, OEMs have been facing financing challenges. Tough financing environment and liquidity concerns continue to impact timely sales.

Published on:

06 July 2021

Published in: NBM&CW July 2021

Share:

We Value Your Comment