India Construction Equipment Industry - Registers 8% volume degrowth in FY22 despite exports growing at 60%

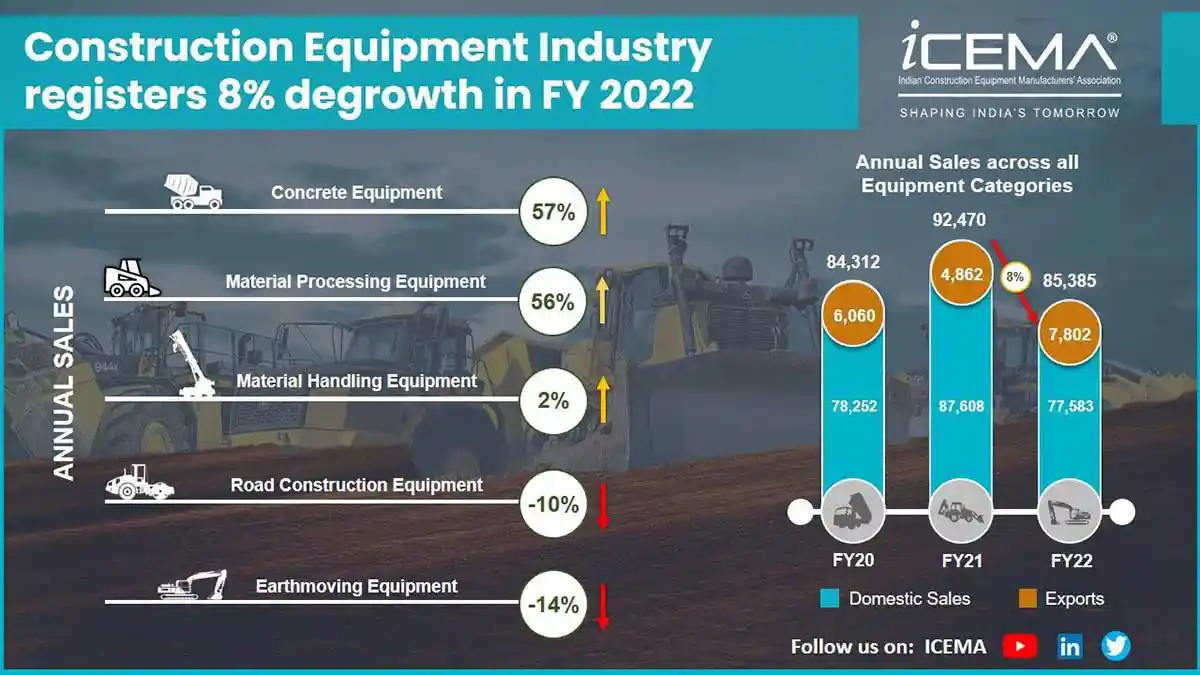

The Indian Construction Equipment (CE) Industry witnessed an 8% de-growth in Financial Year 2021-22 (FY22), with sales having dropped to 85,385 units during the year as compared to 92,470 units of construction equipment sold in FY21.

As per the annual industry data released by Indian Construction Equipment Manufacturers Association (ICEMA), the earthmoving equipment segment which accounts for nearly three-fourth of the total construction equipment sales in India, experienced 14% decline in growth during FY22, while road construction equipment sales were lower by 10% during the same year.

However, the other three segments, namely material handling, material processing, and concrete equipment registered positive growth during the year. Exports of construction equipment also increased significantly by 60% in FY22 over FY21.

There was significant slowdown in the speed of construction of roads & highways in FY22 to 28.64 km/day compared to the much higher pace of 36.5 km/day in FY21. This was a major factor for CE industry de-growth as 40% of the total demand for construction equipment originates from the road sector.

Natural calamities like cyclones and heavy rains also affected construction activity, particularly in the Southern part of the country, further affecting the demand for construction equipment. Sharp increase in input costs due to rising steel and other commodity prices created margin pressures for the CE manufacturers. The industry’s concerns have further accentuated on account of the recent ongoing Russia-Ukraine conflict.

The industry is hopeful of a strong recovery during FY23 on the back of an enhanced export potential and the Government’s continued thrust on infrastructure development such as the National Infrastructure Pipeline, Gati Shakti Masterplan, National Monetisation Plan, and constitution of National Bank for Financing Infrastructure and Development (NaBFID). Several infrastructure projects that have made substantial progress but are facing delays due to financing issues are likely to be given funding priority by the Bank, which, in turn would boost construction activity and create growth opportunities for the CE industry.

The sharp increase in budget outlay on capital expenditure for FY23 by more than 35%, from INR 5.54 lakh crore to INR 7.50 lakh has also given the industry confidence of a quick turnaround for delivering strong growth during the current fiscal. The industry expects a significant increase in award of contracts for highway construction, new railway lines, water management, development of ports, etc. in the current year, while demand for mining equipment which has been quite robust in the last 2-3 years is expected to continue its strong trajectory, aided by favourable global demand for commodities.

Industry leaders feel that the overall future prospect of the industry is positive, as India is entering an exciting era of infrastructure led growth, supported by the Government’s vision of an ‘Atmanirbhar Bharat’ and strong exports push on the back of ‘Make in India for the World’. The journey will further become exciting with the introduction of newer technologies in the industry with the influx of digital and IoT and alternate fuels, which will help the industry attain sustainable growth.

The mood is upbeat as the phenomenal exports growth witnessed by the CE Industry in the last 12 months augurs well for its future sustained growth. With new CEV-IV emission standards now completely adopted by the industry, there are significant opportunities for Indian CE manufacturers to tap into developed markets.

The key recommendations outlined in ICEMA’s Vision Plan 2030 report have helped drive the CE Industry’s interaction with policy makers over the last two years. In the context of a changed global landscape, ICEMA is now working on a revised Vision Plan 2030 to include modified projections and changing trends facing the industry.

Note: The ICEMA Industry Report is prepared with inputs from member companies which represent about 95% of the OEMs operating in the Indian Construction Equipment industry.

Industry views

It is heartening to note the focus of the Government on the creation of Infrastructure through the ‘Gati Shakti’ program in the country. Coupled with these various initiatives, such as institutionalizing of NaBFID to improve liquidity in the system, are expected to create opportunities for growth of the CE Industry. However, the surge in commodity prices, especially steel and diesel along with temporary disruptions in supply chains, need to be addressed if sustained growth is to be expected.

The Indian CE industry has been going through disruptions over the last few years; the stress on account of Covid was compounded by the stress it induced on the global supply chain, which impacted the industry’s ability to respond to pent up demand. As the industry continued to exhibit resilience to come out stronger, the surge in commodity prices and freight charges challenged the industry during FY22.

Yet the industry has managed the crisis to emerge stronger in the spirit of ‘Building India’s Tomorrow’. While last year, the demand across sub-sectors was mixed with some demonstrating strong recovery; overall, the industry growth was muted mainly due to the pace of progress of projects, ongoing commodity price increases, and constrained supply chain.

With the renewed thrust on infrastructure development in the Union Budget 2022, we are hopeful of seeing the beginning of a recovery that would sustain the momentum in the coming quarters to end the current financial year stronger than the past. With Excon 2022 around the corner, which is expected to give a fillip to the industry, we have another good reason to believe that industry will rebound and end the year stronger.

The outlook for FY23 looks promising with a 35% increase in budgetary capex for highway, railway, housing construction, and the Jal Jeevan Mission. We have seen some positive movement in the last few months with an extraordinary push by the government towards road construction. We anticipate that these should help drive growth in the CE industry. The only caveat being that the execution needs to be commensurate to planned outlays.

We foresee a rebound in demand, thanks to the Government’s continued thrust on building world-class infrastructure, which was in fact evident to some extent in the demand offtake firming up in the fourth quarter of the previous financial year.

We are confident about the emergent opportunities and the sector’s growth prospects, supported by the Government’s ambitious programs like Gati Shakti and the National Infrastructure Pipeline. We also expect a significant increase in award of contracts for highway construction, new railway lines, water management, development of ports and others. Demand for Mining Equipment which has been quite robust in the last 2-3 years is also expected to continue its strong trajectory, aided by favorable global demand for commodities.

FY22 started with great hope, however, the decline began in August 2021 leading to an overall muted industry growth. While exports came to the rescue for some manufacturers, overall, 2021 was a challenging year for the industry with regular input cost increases, steel and other commodity price increases which practically doubled by the end of FY22. Added to this, limited availability of funds especially for smaller contractors led to delayed execution / cancellation of orders. In the last quarter of FY22, the third wave of the pandemic and the subsequent Russia-Ukraine war added to the misery of the CE Industry. These challenges were further exacerbated by price increase of bitumen, supply chain issues, non-availability of critical materials and uncertainties. All these challenges will make an immense impact on both the topline as well as the bottom-line of CE manufacturers. Currently, uncertainty continues, and manufacturers are unable to pass on the cost increase to customers. Unless the Government intervenes to soften the input costs, we don’t foresee FY23 to be a great year.

Mitigating the impact of Covid-19, the Indian CE industry registered a 12% growth in 2021 with sales of 82,218 units. While demand was buoyant in the first quarter of 2021, it remained subdued in the second quarter due to the onset of a second wave in early April, and imposition of related lockdowns. Several government investments aimed at infrastructure and transportation aided the rise of the CE industry after the second wave subsided. The residential building segment, as well as the road and mining industries, had a high demand for construction equipment.

The highlight of 2021 was the implementation of a new emission standard (CEV Stage-IV) for all construction equipment vehicles on tyres. Going forward, the price of construction equipment is likely to increase given the rising input material and logistic cost, appreciation of dollar and RMB, and tightening of lending norms and expected liquidity crunch in the near term.

Despite the challenges, the market offers several opportunities including those for small and medium vendors of OEMs given the increasing government investments and push to Make in India strategy. A good monsoon as predicted by the IMD may revive demand in rural and Tier 2/3 townships post monsoon. With INR 6 lakh crore to be released through the National Monetisation Pipeline (NMP) expected to fund the National Infrastructure Pipeline and smoother execution through Gati Shakti Master Plan, the CE market is expected to get a thrust during 2022 and 2023, with a slight dip in 2024 with the general elections.

The Materials Processing segment has seen strong growth in FY 2021-22 driven by a robust demand from the Road Construction segment and also an uptick in Metal Mining activities. Demand from large road construction companies has been stable and there has also been entry of new rental players, which has pulled up demand for crushing & screening equipment in particular. While increased steel prices have helped the demand from Iron Ore Mining companies, the increased costs have also subdued the demand from retail customers to a certain extent. There also has been good growth for equipment coming from Bio Mining and Municipal Solid Waste Processing customers. We expect demand to be strong in FY 2022-23 from both Construction and Mining sectors. However, the cost pressure can bring in some headwinds over the next few months as far as immediate demand is concerned.

FY 2021-22 was about managing challenges on multiple fronts, Covid, supply chain disruption, demand volatility, amongst others. With the recent policy changes and government push towards world-class infrastructure, the long-term industry outlook remains robust, though some volatility is anticipated in the short to medium term. The industry believes in the long-term India growth story in which infrastructure development will play a key role. India has the potential to be a supplier to the world for construction equipment, both at the equipment and the components level.

The demand for machinery for the road sector continues to be slow and the short-term outlook is not very good. However, with the current pipeline of contracts already awarded, the market should start picking up after the monsoons. The mining sector continues to demonstrate good growth and this trend will continue. While the domestic market is flat and down, exports are showing good growth.

India experienced two Covid waves during FY2022: the 2nd wave led to a considerable slowdown in activities and momentum which was going strong since the 2nd half of FY21. Accordingly, the industry saw muted growth in the first three quarters of FY22 resulting in an overall de-growth of 8% for the year. Going forward, we are cautiously optimistic and look forward to growth in FY23 on the back of the Government’s strong thrust on infrastructure development. The biggest hurdle seems to be the unabated increase in input costs/commodities which could be detrimental for the overall growth prospects of our economy as well.

The CE Industry is at the cusp of a unique opportunity: it is emerging out of a tough business phase and entering a sustained demand phase. Higher input cost resulted in higher owning cost for customers and proved to be a dampener for demand. FY2022-23 will be a year of improving demand, and manufacturers will have to constantly work on smarter product offerings and lower cost structures. We are looking forward to an exciting year ahead for the industry.

What is the overview of the CE industry in FY22 and the outlook for FY23?

If you compare the FY21 and the FY22 figures, there is not much change despite the market compressing by 8%. Earthmoving and road construction have registered a slightly negative growth but material handling, material processing and concrete construction equipment have done well.

If we analyze the quarterly development between Q1 and Q4 of the last fiscal, we can see that the year improved progressively. Q1 was slow because of the second wave of the pandemic, while Q2 and Q3 picked up pace slowly due to the extended monsoon and the CE Industry’s transition to CEV IV. But in Q4 we saw the market getting a boost with much better after-sales business.

Another factor that has impacted sales of construction equipment is the stagnation in rental rates. People are probably using older machines and wanting to retain their fleet for longer usage. Sales of compaction machines and backhoe loaders are, therefore, not happening. Sales of concrete equipment and mineral processing were reasonably good due to metro and high-speed rail projects and a pick-up in the real estate sector.

In the mining sector it is a completely different story with demand outstripping supply. We will continue to see this trend this year and in the next. However, availability of components and raw materials for mining equipment continues to be a challenge even in global markets where short supply is not meeting the demand.

In road projects, there is a lot of activity on the ground, but it is not enough to meet our ambitious target of 25,000km. To achieve this, a project pipeline has to be in place. In March, we achieved tendering of 5000km of roads in a single month, which is very good compared to 11,500km done in all of last year.

The pace of road construction in the first three quarters was low but in the last quarter of FY 22 we witnessed good progress. In January, it was 25km/day, followed by 48km/day in February, and in March, it was a whopping 77km/day. The reports of the ministry are in line with our observations.

Outlook for FY23

FY23 is going to be a very strong year for the construction equipment industry in view of the Budget FY22-23, in which the Government has increased the allocation by 35% for infrastructure development, construction of 25,000 km national highways, along with railways, river linking projects, etc. So, we anticipate 20% growth or more in the CE Industry.

Overall, the market will be strong for the next year. We expect September to December to see stronger demand. The government also wants to implement a lot of projects this year as there will be elections in 2024. Additionally, the general economy is also doing quite well.

What factors and industry issues are impacting the construction sector?

The world has changed dramatically: there is an energy crisis, shortage of raw materials, shortage of skilled workers and so on. Changes will not happen suddenly in our favour, nor will they go away if we ignore them; so we must acknowledge this reality and find the right solutions.

There are dampening factors like rising inflation which will affect interest rates. Cost of raw materials like steel and cement have gone up drastically. Steel costs have gone up by 100% which will impact infrastructure project developers and contractors as well as the CE industry since our machines are made of 90% iron. Freight costs have also gone up around the world. There are issues of sustainability, climate change and pollution in the environment which have increased the focus on emission norms, electrification, and the use of alternate fuels.

Another major issue is land acquisition which is seemingly unlikely to change, and neither will the laws change suddenly. But if our target is to achieve 25,000 km of road construction in this fiscal, then the size of the projects pipeline must increase, i.e., the number of projects that can be pushed together has to be increased. Award rate must be higher at around 30,000km. Additionally, since we have rains for three months in our country, construction must happen in the remaining 9 months. There needs to be a greater focus on ensuring cash flows as there are a lot of players (developers, contractors, rental equipment users) struggling to collect money through bank loans, NBFCs, and leasing.

The Industry needs to raise these issues with the government which must come up with solutions that will have a favourable impact on all the stakeholders, especially customers and contractors. If the Government does not address the issues, then projects could become unviable and lead to huge losses. And if the larger aim of infrastructure development & sustainable development is not met, the roadblocks are not removed, and the problems are not addressed, then our country will not progress at the rate that it can.

How can the cost of construction be brought down in view of the high cost of fuel?

We, as an industry, took the initiative last year to encourage adoption of biodiesel. Shifting to biodiesel by supporting the biodiesel industry could bridge the demand and cost concern. Currently, investments in biodiesel plants are very low. It has to be made more easily available for bulk consumers.

There are two things that could encourage adoption of biodiesel: quality of the diesel has to be consistent and supply has to be continuous and steady. We are aware that B7, B20, B30 can be used and in some cases B100 is also working. In addition, end-users need more clarity on alternate fuels like biodiesel.

There are countries which have adopted biodiesel in a big way. In Indonesia, B30 is mandatory; and in Sweden, B30, B35 and HVO are being used. Petrol pumps in India are supposed to provide B7 as standard diesel but its adoption is barely 1%.

Electrification and Hydrogen are going to be future alternatives. At EXCON, visitors can view OEMs machines with biodiesel blends. EXCON always gives a push to the industry and the market to forge ahead with better machines and solutions.

What impact do you see on the CE industry in view of the Russia – Ukraine war?

Global demand is very strong for equipment and there is a huge backlog in European factories of almost 9-18 months. For India, it is a good opportunity in intermediate parts manufacturing. Indian government’s PLI and Make in India initiatives have made India a good destination for setting up new factories. This can be seen from the number of new companies entering the Indian market.

What message would you like to give stakeholders in the infra Industry?

This period is India’s moment. It is for us to utilize it. We must take responsibility to improve the stature of our country globally. Today, we are able to stand up and voice our views on global platforms and the world listens and respects our views.

We are progressing in digitalization, infrastructure development, GDP growth and market capitalization. Our relevance in the world is much more than what it was 20 years ago. We should take our country to the next level of growth in sectors like healthcare and transportation by developing strong and sustainable infrastructure. Many sectors are making the right moves towards growth and we must keep the momentum going.

Today, people want to do big projects; fleet owners have grown 1000 times more than what they were 20 years ago. Small operators are doing 100 million cubic meters of earthmoving every year. The government is also keen to step up the infrastructure construction activities.

In the budget for 2021-22, the government has announced an outlay of Rs 1.97 trillion for the PLI (production liked incentives) scheme for 13 sectors including telecom, automobiles & auto components and steel, among others. Schemes like PLI, Component Champion and Global sourcing will encourage both CE domestic & global players to ramp up investment in India. They will help attract global manufacturers especially from EU, Japan, and Korea to set up their manufacturing base in India. Such schemes will also propel exports to 15 to 20 % of production.

Instead of focusing on small issues that are regressive for the country’s progress, we must focus on important matters which will take us forward. Some of the obstacles will remain and will not be easy to sort out. Gati Shakti, for instance, aspires to make things smooth but it will not happen overnight. However, the direction is set and we should believe in it and act on it. I would like to believe that everyone in the country has this confidence and vision.

CE Industry Suggestions/Recommendations for the Government

Sustained Demand CreationRobust Operating Ecosystem

- Slowdown in construction activity be addressed through speedy implementation/execution of infrastructure projects announced by the Government under the NIP and Gati Shakti Masterplan.

Technology and Skilling

- Improve access to low-cost funds by expediting implementation of announced DFI, enabling access to low-cost funds for both Banks and NBFCs by providing priority sector status to CE industry or at par with the infrastructure sector to attract long term investments and speedy implementation of NMP

- Schemes like PLI, Components Champion and global sourcing for CE Industry to be introduced to help attract global manufacturers especially from EU, Japan and Korea to set up their manufacturing base in India.

- Reduce cost of doing business through lowering logistics cost and optimising input cost

- Create single-point Nodal authority (across relevant ministries, directorates) to finalize and notify relevant norms and regulations for CE industry. MoRTH is well-equipped to be the proposed nodal authority.

- Emission norm regulations for off-highway construction equipment be introduced; an inter-ministerial task force be formed for implementation of the regulations for off-highway equipment, this will open up export opportunities for this segment.

- Certification of operators to be made mandatory for operating all types of Construction Equipment, to ensure higher levels of safety, efficiency and quality.

Published on:

11 May 2022

Published in: NBM&CW May 2022

Share:

We Value Your Comment