Construction Equipment Industry Stable, Despite Multiple Headwinds

ICRA’s outlook on the CE industry remains stable in the backdrop of the government’s policies and programs for the infrastructure sector, with its capex being a key driver for the Equipment industry.

Construction equipment (CE) industry volumes dropped by 60% in Q1FY2021 because of Covid 1.0 and aligned restrictions. However, with the government’s focus on infrastructure sector, demand picked up again, and the industry reported a 13% increase in volume for FY2021, supported by a strong increase in volume during H2FY2021.

After having one of its best quarters in terms of volume in the fourth quarter of FY2021, the Indian construction equipment industry faced multiple headwinds in FY2022. During the first quarter of fiscal year 2022, the volume of the industry was impacted by restrictions related to Covid 2.0 and a temporary slowdown in road construction. Demand also slowed because OEMs raised their prices to offset higher costs caused by changes in emission rules and higher prices for inputs, whereas rentals of CE operators remained flattish, thereby exerting pressure on the income of CE buyers.

Steel is one of the major constituents of the CE segment’s raw material cost. Increased steel prices apart from elevated charter rates, and rupee depreciation has exerted cost-side pressures amid high import dependence thereby leading to an increase in CE prices. This is further exacerbated by new emission norms (CEV-III to CEV-IV from October 1, 2021) for which a 10-15% hike in prices of the new compliant CEs is seen.

The overall increase in the cost of ownership following a rise in prices of equipment and stagnant/muted rentals kept the buyers at bay during the last fiscal. Negative operating leverage because of a decline in volume along with input cost pressure acts as a double whammy for the industry’s profitability, with most players witnessing margin contraction during FY2022. CE players remain dependent on imported components, with the share in certain segments like excavators remaining as high as 40-50%. There has been some moderation in steel prices in recent months, though the depreciation of the rupee will partially offset the benefits of commodity price easing for industry participants.

In Union Budget 2023, the Centre’s capex is budgeted to rise by 24.5% to Rs. 7.5 trillion in FY2023 BE, relative to FY2022 RE, while the combined capital outlay of 18 states is budgeted to rise by 14.5% to Rs. 5.0 trillion in FY2023 BE from Rs. 4.3 trillion in FY2022 RE. Capital expenditure in key infrastructure segments like Railways, Roads and Highways, Metro and MRTS projects, and drinking water supply has also seen growth in allocation.

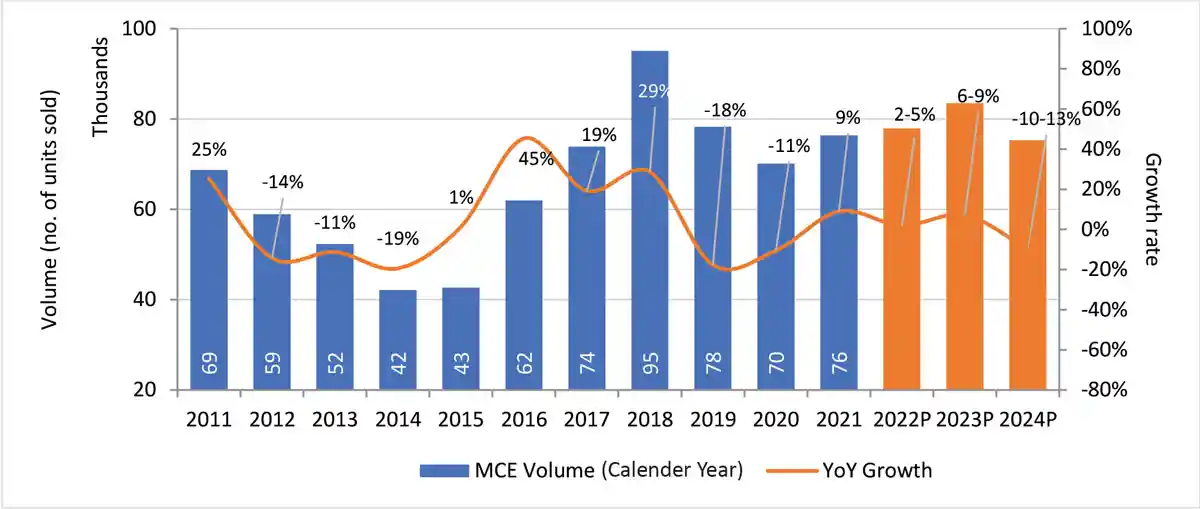

Source: ICRA Research; volumes for earthmoving (backhoe, excavators, wheeled loaders, skid-steer), road construction (compactors, pavers and motor graders), material handing (PNC) and mining (dumpers and dozers). P = ICRA Projected volumes

Source: ICRA Research; volumes for earthmoving (backhoe, excavators, wheeled loaders, skid-steer), road construction (compactors, pavers and motor graders), material handing (PNC) and mining (dumpers and dozers). P = ICRA Projected volumesAdditional allocation to the PM Awas Yojna will also favour the overall growth of the construction industry and, in turn, the CE industry. Further, the scope of the National Infrastructure Pipeline (NIP) now includes 9,335 projects (from 6,835 projects at the time of launch), with total envisaged investments of Rs 111 trillion during FY2020-FY2025. The state government also plays a critical role in the National Infrastructure Pipeline (NIP), with 40% of overall Rs. 111 trillion expected to be invested by the states.

With the decline in revenues, many state governments have resorted to lower-than-required infrastructure spending over the last two years. In this context, the proposal in the Union Budget 2022-23 to provide assistance in the form of loans to states for capital expenditure and increase the allocation to Rs.1.0 trillion in FY2023BE from Rs.150 billion in FY2022 RE is a positive sign. This is expected to provide more headroom to state governments for increasing the capex. Overall, higher capex by the centre, and support towards states could help in improving the pace of Infrastructure investment and remain positive for creating a sustained demand for the mining and construction equipment industry, which witnessed a slow pace in the earlier fiscal.

Overall, ICRA expects muted volume growth of 2-5% in CY2022 for the mining and construction equipment (MCE) industry, due to the high base effect of H1CY2021 and near-term headwinds on demand. The volumes are expected to pick up in H2 CY2022 supported by infrastructure thrust in Union Budget 2022-23 and expected to pick-up in infrastructure activity ahead of the elections in 2024.

When compared with growth on a calendar year basis, the growth rates are contrasting when assessed on the fiscal year (Apr-Mar period), due to the exceptionally strong Mar-2021 quarter last year. While the volumes moderated by 17%1 in FY2022, ICRA expects a 12-15% YoY growth in FY2023. Though the elevated commodity headwinds and increased freight rates will weigh on the profitability of CE OEMs, the recent correction in prices of steel will provide some respite, post the prices are reset for most of the players (likely from Q2 FY2023).

Further, the improved operating leverage benefits in the backdrop of expected 12-15% volume growth in FY2023 should also help to offset cost pressure. Many OEMs have already taken sequential price hikes in the last twelve months (in the range of around 5-10%) and a further hike in the current fiscal is expected to largely offset the cost pressure. ICRA Research expects the operating margins to sequentially improve in FY2023 but will remain below pre-Covid levels, and it may take another two years for the industry to reach normalcy in terms of operating profitability.

Published on:

13 July 2022

Published in: NBM&CW July 2022

Share:

We Value Your Comment